Do you choose the resale market or opt for a pre-construction home? When you are in the market to buy a home, it is an important consideration. There is no doubt that pre-construction homes have a certain appeal to homebuyers.

Buying brand new provides the opportunity to own a home that no one else has ever lived in. And because the house is in the pre-construction phase, you have the opportunity to customize it to your preferences.

If pre-construction is something you’re considering, here’s the info to help you decide if it really is for you.

What is a Pre-construction Home?

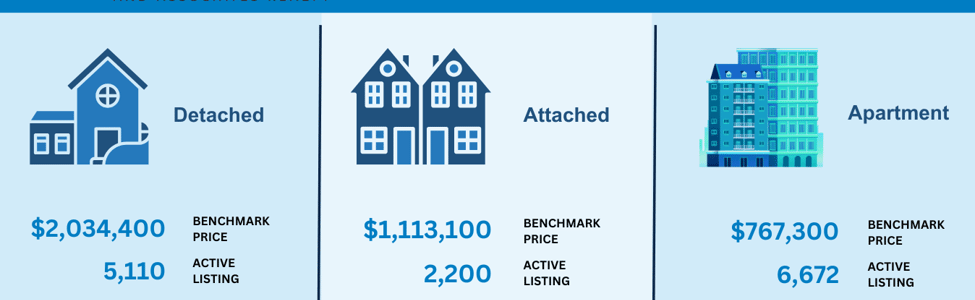

A pre-construction home is exactly what it sounds like: a house you buy before it has been constructed. Most styles of homes are available for pre-construction buying, including:

- High-rise condos

- Low-rise condos

- Detached houses

- Semi-detached houses

- Townhouses

For a condo development, you’ll buy a home from blueprints or a 3D computer rendering that provides a simulated walk-through. For houses, you can usually visit a model home that sits on the lot of the future development. Although model homes tend to be highly aspirational in their decor, it’s your chance to get a more realistic look at what you’ll be buying.

What to Consider When Buying a Pre-construction Home

The Process of Buying a Pre-construction Home

If you’re wondering, how buying a pre-construction home works, imagine buying a property that hasn’t been built yet. It gives you some flexibility but also comes with risks. Whether you’re considering pre-construction detached homes or condos, you’ll pick your home based on blueprints or 3D renderings. Keep in mind that developers might make small changes to the layout as they build.

Are pre-construction homes cheaper? These properties are often priced lower because developers offer discounts to attract early buyers and secure funding. However, you also need to account for potential costs like upgrades, closing fees, and any unexpected changes in construction timelines. Pre-construction homes often come with flexible payment plans, where buyers make incremental payments during the construction phase. After signing the purchase agreement, these payments are non-refundable. The timeline for new pre-construction homes can take months or even years, and delays are common due to things like weather, supply chain issues, or market changes. Locking in your price early can be great if home values go up, but if the market cools, you could end up paying more than it’s worth. Be aware of these risks and have a backup plan if delays drag on.

Blueprints and Renderings

When buying pre-construction detached homes or condos, don’t just rely on blueprints and renderings. Developers often use wide-angle lenses and special lighting to make spaces seem bigger than they are. If you can, visit a model home to get a better feel for the real size and layout, but remember that models are often packed with upgrades that won’t be included in your standard unit. Pay attention to things like ceiling heights and window placement, which can make a big difference in how open the space feels. Also, with new pre-construction homes, ask about possible changes to finishes or materials—what you see in the renderings isn’t always guaranteed, especially with potential supply chain issues. Make sure you get these details in writing to avoid surprises later.

Interim Occupancy for Condos

For condo buyers, interim occupancy happens when the building is ready for you to move in, but it hasn’t been officially registered, so you don’t fully own the unit yet. During this time, you’ll need to pay occupancy fees that cover things like maintenance and taxes, but they don’t count toward your mortgage. Many buyers don’t realize this phase can last longer than expected, depending on how quickly the developer finishes the registration. If you’re buying pre-construction homes, you may also face restrictions on renting out your unit or making changes during this period, so it’s important to check with the developer about what’s allowed. When figuring out how to find pre-construction homes, make sure to factor in these extra costs and any potential restrictions when planning your budget.

Assignment Sales

With pre-construction homes, you can sell your contract before the property is built through what’s called an “assignment sale.” This is a good option if your circumstances change and you need to back out, as it lets you transfer the purchase agreement to another buyer. However, assignment sales often come with extra terms, like needing the developer’s approval, and they may charge additional fees or limit how much profit you can make on the sale. Some developers even restrict assignment sales altogether or only allow them after a certain stage of construction, so check these details in your contract. Also, assignment sales can be trickier to market since buyers may need to cover your original deposit, making it less appealing to some.

Tarion Warranty Protection

In Canada, new pre-construction homes are covered by the Tarion Warranty, which protects you from issues like construction defects, structural problems, and delayed occupancy. The coverage is broken down into different time periods—one year for general defects, two years for things like plumbing and electrical systems, and seven years for major structural issues. What some buyers don’t realize is that it can also cover problems like water leaks or even landscaping defects, depending on what’s in your agreement with the builder. The warranty isn’t automatic. You need to file a claim within the covered time frames to get repairs. Also, check if your province has slightly different warranty protections, as it can vary.

Price Adjustments and Escalation Clauses

Some contracts for pre-construction homes have escalation clauses, which let the builder raise the price if material or labor costs go up during construction. These increases can happen for reasons like inflation or supply issues, and there’s not always a limit on how much the price can rise, so the final cost could end up being more than you expected. Escalation clauses are more common when the economy is uncertain. In some cases, the increase might only apply to certain materials, while in others, it could be broader. You can try to negotiate the clause or ask for a limit on how much the price can go up. Be sure the builder explains how they’ll notify you of any changes, and have your lawyer check the details so you’re not caught off guard.

The Benefits of Pre-construction Homes

So, what’s the big attraction of a pre-construction home? There are quite a few benefits, including:

Warranty

Like buying a new car, a brand-new home comes with a warranty. The warranty programs in Canada offer protection for newly built homes, including delays in occupancy and closing coverage, protection for your deposit, and the cost of repairs should there be issues once you move in.

Lower Price Tag

Are pre-construction homes cheaper? Pre-construction homes can offer better value than the resale market because you’re essentially buying a promise. You put down your deposits (as per your purchase agreement), and the builder promises to deliver a home by a specified date.

No Bidding Wars

Depending on where you’re shopping for your home, bidding wars can raise the price. When inventory is low, buyers are desperate, and the more attractive the home and neighbourhood, the more chance you could end up paying an inflated price for a resale home. When it comes to pre-construction, you’re looking at a set price. You’ll know exactly how much you’ll pay, usually at fair market value.

Designer Home

You have the option of designing your home with plenty of upgrades available. There are not only upgrades for finishings like kitchen counters and flooring, but you can often make structural upgrades, including adjusting some floor plan options.

Because you’re making all your decisions during the building process, they are far more affordable than a reno or upgrade once you move in. The pre-construction process allows you to make smart decisions that will increase the resale value of your home.

Lower Condo Fees

When buying a brand new condo, the condo fees are lower in new builds than in resale condos. That is because everything is new, and the management has yet to see how much it costs to operate the building or property, so, as you will read below, this can also become a drawback.

Flexible Deposits and Down Payments

Although you tend to need more for a deposit or down payment for pre-construction, the payments are staggered. You have time to keep saving as there is a small amount paid upfront, and the rest is paid on a schedule that leads up to the final closing.

Better Choices

You’ll have more choices when buying pre-construction compared to resale condos, such as the floor and the location of your unit (i.e., a corner unit or a better view).

10-Day Cooling Off Period

You’ll have ten days to “cool off” and reconsider your purchase. You can arrange for financing and have a lawyer review the agreement during this time. Should you change your mind or find something in the deal you don’t like, you can get your full deposit back and walk away.

The Downside of Pre-construction Homes

As with everything, you have to take the bad with the good. Some downsides to pre-construction include:

Delays

You should always go into pre-construction with a hint of pessimism. The reality is that you could face delays. And we’re talking years, not weeks or months. Researching developers will help you find a trusted company with a good reputation for customer satisfaction, hopefully lessening the likelihood of delays.

Condo Fees Rising

Although you’ll see lower condo costs going in, you must prepare to see an increase of as much as 10 to 20 percent within two years. It takes about two years for the management to realize the cost of running the condo, and increases are always required. This has to be added to your monthly budget when determining if you can afford your new condo, or you might have trouble making ends meet.

Higher Deposits

While you do get the opportunity to stagger your deposit payments, you will be paying as much as 10 to 20 percent overall, compared to a deposit of five percent when signing a resale agreement. In most cases, you’re looking at a five-per-cent sales deposit up front and then payments at four, nine and 18 months, depending on the developer or building schedule.

Mortgage Challenges

When buying a resale home, you’ll usually be making your purchase before your locked-in rate expires. However, this can be a challenge for pre-construction homes if the home completion date is extended and passes your locked-in expiry date.

Occupancy Fees

In the case of a pre-construction condo, there is a registration process required before you can legally own your unit. If you have to move in before registration is complete, that is called interim occupancy. You pay a monthly occupancy fee if you move in during this period, which does not go towards your mortgage. This monthly fee will include your condo fees, the interest portion of the balance owing on the purchase price, and a portion of your property taxes.

Project Cancellation

When you buy pre-construction, you risk the project not making it to the finish line. Whether it’s a lack of sales or rising construction costs, pre-construction cancellation is a reality for many homebuyers. Sure, you get your money back. However, the money you invested in the project has not earned you anything. You could have used it toward another pre-construction development or an alternative investment. On top of that, you originally purchased at an earlier year’s price. That money now has to go toward today’s real estate market, which may have risen sharply, leaving you with less buying power.

Other Pre-construction Costs

Your pre-construction home also has additional fees, including GST/HST. There are rebates available if the house is your primary residence, depending on your province.

You’ll face some taxes (that you won’t be too thrilled about) if you intend to rent your unit. A good way to avoid these taxes is to live in your unit for a while before renting it out.

There are also closing costs you don’t have when buying a resale home, such as charges for utility meter installations, fees to track your deposit payments, electronic land registration system usage, and more.

These additional fees can add up to as much as three percent on top of your purchase price. Working with a real estate agent and lawyer will help you get a more realistic view of what further costs you’ll have to pay on your pre-construction home. A real estate agent can also help you look at a variety of resale and pre-construction options so that you are sure to find your dream home.

How to Buy a Pre-construction Home?

You can take steps to maximize the benefits and minimize the risks of buying a pre-construction home. If you are wondering how to buy a pre-construction home, first research your builder. Visit online directories to determine if you are purchasing from a reputable builder. You’ll want to know that they have a record of completing projects so that you can be confident that you are investing your money wisely.

Next comes the purchase agreement. You must understand the agreement before you sign it. It is a legal and binding contract, so you must have your lawyer review it before you sign on the dotted line. This review is your chance to understand the warranty coverage on the home better. You are buying a new home, so some parts of your home are covered after you purchase it, making it essential that you understand what is covered and for how long.

Speaking of lawyers, some legal professionals specialize in pre-construction homes and are a real asset in the buying and negotiation phase. They know what to be on the lookout for and can guide you. On top of being a significant financial investment, it also requires a more extended buying period, so it’s best to have someone experienced by your side.

Finally, you will need to prepare for your pre-delivery inspection. Before you take possession, you can walk through your new home and ensure that the house is delivered to you as was agreed. You can reference pre-delivery checklists to ensure you are looking for the right things.

Completions Are Slowing

Over the last year, a new trend has formed in the Canadian real estate market: Residential construction activity is taking too long to build. Whether because of a tight labour market or rocketing interest rates, single-family homes and condominiums are being completed at a snail’s pace. Today, it takes approximately five to ten years before a residential development is ready to move into – it is usually around 18 months before a single-family home is completed – and the current trends are becoming riskier for developers.

While housing starts are higher than they were before the coronavirus pandemic, it is taking so long to deliver new projects to the market due to the plethora of simultaneous projects underway. As a result, the lengthy delays could exacerbate Canada’s affordability challenges because the country will be unable to construct the roughly 5.8 million homes it needs in seven years.

The delay in construction has also affected homebuyers in myriad ways.

Industry experts argue that homebuyers are not closing their transactions and walking away from enormous deposits. The reason? Interest rates have soared to their highest levels since before the Global Financial Crisis, meaning buyers cannot qualify for a mortgage when the closing date nears. This is especially troublesome if prices continue their growth from the coronavirus pandemic.

Reports suggest that some deposits are as high as $320,000.

Before buyers think they can abandon their purchase without any repercussions, legal experts say that builders can seize the deposit and sue for any damages. Additionally, if the developers resell these properties for less than what the original buyers acquired them for, builders can return to the party and request a difference in the cost.

“While some new launches with competitive price points have seen success, many projects have been unable to make an economic case for proceeding in the current market, causing more supply to be put on hold,” said Shaun Hildebrand, president of Urbanation, in a report. “As pre-sale activity typically impacts construction starts with a 12-18 month lag, the slowdown in new condo sales that began in the second half of 2022 is expected to continue weighing on construction starts in the coming quarters.”

Ultimately, the Canadian real estate market, notably in the major urban centres, is beginning to witness two trends: a pile of empty homes and developers abandoning projects.

New to Pre-construction Homes? Get The Help You Need

Knowledge is key to moving through the pre-construction process, especially if it is your first time. An experienced real estate agent can help you right from the start. From analyzing market data to understanding the purchase price, a real estate professional understands your local market and can guide you throughout the process.

Having a real estate agent guide you when buying pre-construction homes can make the process much smoother. They help with contracts, negotiating terms, and understanding details like escalation clauses and interim occupancy. Agents also know how to find pre-construction homes that suit your needs and budget. If you’re wondering “How does buying pre-construction homework?” a RE/MAX Michael Cowling and Associates agent can walk you through every step so you’re well-informed and protected throughout the process.

If you're navigating this dynamic market, whether buying or selling, let's talk strategy. Our team can guide you through the most efficient processes, aiming to save you time, money, and hassle. Contact us today and let's make your real estate journey a success!

Source: RE/MAX.ca